Testimony

before the

Senate

Committee on Banking,

Housing and

Urban Affairs

Reasonable Expectations for

Transit in the Modern Urban

Area

8 October 2002

Wendell Cox

Visiting Fellow

The Heritage Foundation

&

Principal,

Wendell Cox Consultancy

Reasonable

Expectations for

Transit in the Modern

Urban Area

Testimony by Wendell

Cox

Before the

Senate Committee on Banking,

Housing and Urban Affairs

Senate Banking, Housing & Urban Affairs Committee Hearing Notice

Mr. Chairman and Members of the Committee:

Thank you for inviting me to testify today.

My name is Wendell Cox. I am an independent consultant

headquartered in Belleville, Illinois,

in the St. Louis area. I am also a

visiting fellow at The Heritage Foundation. I must stress, however, that the

views I express are entirely my own, and should not be construed as

representing the position of The Heritage Foundation.

I was appointed to three terms on the Los Angeles Country

Transportation Commission by Mayor Tom Bradley and was appointed to the Amtrak

Reform Council by Speaker Gingrich. Earlier this year I served an assignment as

a visiting professor at the Conservatoire National des Arts ET Metiers (CNAM),

a French national university in Paris,

conducting seminars and research on urban planning and transport.

I will share perspectives that you may not have heard before

--- about how transit has little or no potential to address traffic congestion

and how so-called “smart growth” promises to worsen traffic congestion while

making housing less affordable especially for the nation’s lower income

households who are disproportionately minority. These views are held by other

professionals and academics as well, and they challenge what is considered to

be the conventional wisdom in both transport and urban planning. I will, of

course, be pleased to supply the Committee with additional details as

requested.

Increasing Traffic

Congestion, Declining Transit Market Share

It is painfully obvious to commuters in virtually all US

urban areas that traffic is getting worse. This has been going on for some

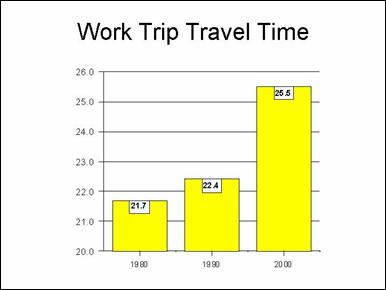

time, but has become much more critical in recent years. For example, the US

Census Bureau reports that average work trip travel time increased 3.1 minutes

nationally from 1990 to 2000, a rate four times that of 1980 to 1990. And,

things are likely to get much worse (Figure #1).

For some time there has been a widely held view that transit

has the potential to reduce urban traffic congestion. Indeed, that sentiment

was part of the rationale behind making highway user fees available to transit

in the 1982 reauthorization.

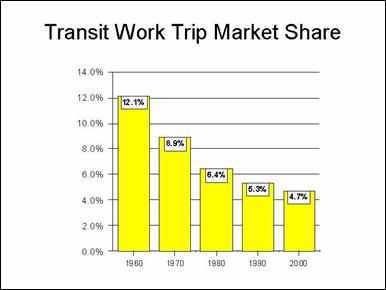

Yet, despite spending nearly $500 billion in subsidies at

the federal, state and local level since 1960, transit’s share of urban trips

has continued to trend downward. This is confirmed by the 2000 Census, which

shows that transit’s share of work trips has reached a new low --- 4.6 percent

(Figure #2), down more than 10 percent from 1990 (Table #1). While employment

was increasing 13.2 million, transit work trip use declined nearly 23,000. Only

two metropolitan areas with more than 1,000,000 population maintain a transit

work trip market share of more than 10 percent (Table A-1).

|

Table #1

Work Trip Market Share by Mode: 1990 & 2000

|

|

Mode

|

1990

|

Share

|

2000

|

Share

|

Change

|

Change in Share

|

|

Car, Truck or Van

|

99,592,932

|

86.5%

|

112,736,101

|

87.9%

|

13,143,169

|

1.5%

|

|

Drove Alone

|

84,215,298

|

73.2%

|

97,102,050

|

75.7%

|

12,886,752

|

3.4%

|

|

Car Pool

|

15,377,634

|

13.4%

|

15,634,051

|

12.2%

|

256,417

|

-8.8%

|

|

Public Transit*

|

6,069,589

|

5.3%

|

6,067,703

|

4.7%

|

(1,886)

|

-10.3%

|

|

Public Transit

|

5,890,155

|

5.1%

|

5,867,559

|

4.6%

|

(22,596)

|

-10.6%

|

|

Taxicab

|

179,434

|

0.2%

|

200,144

|

0.2%

|

20,710

|

0.1%

|

|

Motorcycle

|

237,404

|

0.2%

|

142,424

|

0.1%

|

(94,980)

|

-46.2%

|

|

Bicycle

|

466,856

|

0.4%

|

488,497

|

0.4%

|

21,641

|

-6.1%

|

|

Walk only

|

4,488,886

|

3.9%

|

3,758,982

|

2.9%

|

(729,904)

|

-24.9%

|

|

Other

|

808,582

|

0.7%

|

901,298

|

0.7%

|

92,716

|

-0.0%

|

|

Work at Home

|

3,406,025

|

3.0%

|

4,184,223

|

3.3%

|

778,198

|

10.2%

|

|

Workers 16 Years &

Over

|

115,070,274

|

100.0%

|

128,279,228

|

100.0%

|

13,208,954

|

0.0%

|

|

Source: Data from US

Census Bureau

*With Taxicab

|

Figure 1

Figure 2

The Transit Dilemma:

Little Auto Competitive Service

This is not to suggest that transit does not play an

important role. Make no mistake about it --- where transit provides

auto-competitive service, people use it. To be auto-competitive, transit must

be, at a minimum, time competitive with the automobile. The 2000 Census data

indicates that transit work trips take considerably longer than auto work

trips. The average transit work trip was 43 minutes, which compares to other

modes (mainly auto) at 24.8 minutes. Transit work trips take longer than auto

trips in all metropolitan areas with more than 1,000,000 population (Table

A-2).

But where transit is auto-competitive, it is very

successful. For example:

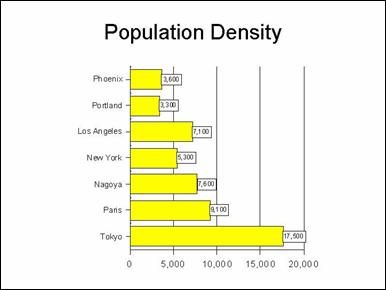

- In the

Tokyo area, nearly 60 percent

of travel is on transit. Why? The reason is that transit is generally

faster than the automobile, with the dense network of urban rail services

and frequent connecting bus service making transit service attractive

throughout the urban area. This is illustrated by the fact that Tokyo,

with approximately 1.5 times the population of the New

York urban area, carries approximately 4.5 times

as many riders annually, and 60 percent more riders than all of the

transit systems in the United States

combined. Nonetheless, the automobile is making significant inroads in the

Tokyo area. In suburban areas,

where the auto is more competitive, transit market share is nearly 40

percent below that of the central city. And, throughout the area, transit

market share has fallen nearly 30 percent since 1970.

- In the

Paris area, 24 percent of

travel is by transit. There, the commuter rail and metro systems provide

generally faster travel than the automobile, with more than 60 percent of

central city oriented travel on transit. But the situation is much

different in the suburbs, where 80 percent of Parisians live and work.

There, only 15 percent of travel is on transit, because transit provides

little suburb to suburb service that is auto-competitive. As in Tokyo,

transit’s market share has fallen in the Paris

area, approximately 40 percent since 1970. The situation and experience in

Paris is typical of other

urban areas in Western Europe.

- In the

New York area, approximately

10 percent of travel is on public transit. Much of this travel is focused

in the city of New York, and

especially to the Manhattan central

business district (below 59th Street).

In 1990, approximately 75 percent of work trips to this area were on

transit. In fact, approximately 22 percent of the nation’s transit work

trips were to the Manhattancentral business district, an area of less than

10 square miles. Nearly 73 percent of work trips to locations within the

city of New York were on

transit, representing more than one-third of the nation’s transit work trips.

Yet, in the vast sprawling suburbs of New York,

only four percent of work trips were by transit. The difference is that

substantial levels of auto-competitive service is provided to Manhattan

and within the city of New York.

It is possible to provide auto-competitive service because of the city’s

high population and density, and the slower automobile operating speeds

that result from the intense traffic congestion. Other than travel in and

to the city, however, few trips can be made by auto-competitive transit.

- Transit

accounts for more than 50 percent of work trip travel to the Chicago

central business district, the nation’s second largest downtown. Again,

the key is auto-competitive service available to this concentrated area

from most locations in the urban area. Within the city itself, transit’s

work trip market share is nearly one-third. But in the suburbs, transit’s

work trip market share is barely three percent. Travel by transit from

suburban residence to suburban employment locations can average more than

two hours, in an urban area where automobile work trips average less than

30 minutes.

- In

most other major metropolitan areas, transit competitive service is

largely limited to downtown locations, and often only during peak

commuting hours. Outside the New York

and Chicago metropolitan

areas, overall transit market shares tend to be approximately one percent

(Figure #3)

Figure 3

What all of this says is that transit is largely about downtown

and to a lesser degree a small number of urban cores (Figure #4). Overall, only

the New York and Chicago

metropolitan areas maintain a transit work trip market share of more than 10

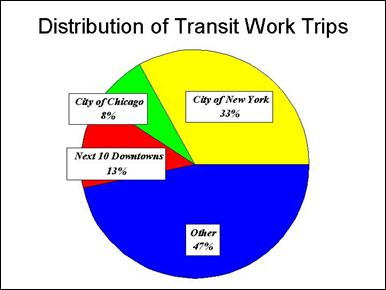

percent, with most of that concentrated in the core areas. In fact, more than

one-half of the nations’ transit work trips are to locations within the central

cities of New York, Chicago

and the ten next largest central business districts. Thus, 3.1 million of the

nation’s transit work trips are to a gross area of less than 600 square miles,

while the balance of 2.8 million transit work trips are to the other more than

86,000 square miles of urbanized land. Thus, outside trips to downtown, transit

is able to make little or no difference with respect to traffic congestion.

In most major metropolitan areas, auto-competitive transit

service is limited to downtown service. This is illustrated by Portland

(Oregon), which has the nation’s

most aggressive smart growth policies and has nearly doubled transit service in

the last decade. Transit competitive service is provided from approximately 70

percent of the urban area to downtown (where transit competitive is defined as

1.5 times auto travel times). Outside downtown employment locations are

accessible to only five percent of the urban area by transit competitive

service. People are not going to forsake their cars for transit service that

takes too long, or transit service that doesn’t even exist.

Figure 4

It is not surprising, therefore, that people who use transit

to non-downtown locations have much lower incomes than those able to access the

auto-competitive services to downtown. In 1990, downtown transit commuters had

an average household income within six percent of the national average.

Non-downtown transit commuters had an average household income 40 percent below

average. It would appear that transit is used for non-downtown work trips only

by those who don’t have a choice (those who have no automobile available).

The key to getting people out of their cars is to provide

automobile competitive service --- service that is competitive in travel time.

But, as noted above, there is little auto-competitive service in the United

States and little more planned to areas

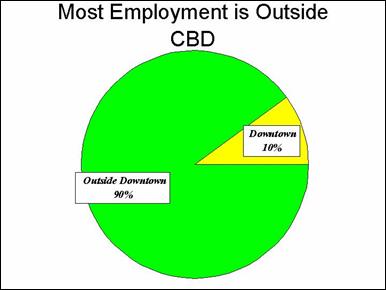

other than downtowns. And, despite their vertical impressiveness, downtowns

represent a small and declining share of metropolitan employment in the United

States. In 1990, the average downtown area

accounted for barely 10 percent of metropolitan employment (Figure #5). Even Manhattan’s

central business district, the second largest in the world, accounted for

barely 20 percent of metropolitan New York’s

employment.

Figure 5

The Union of International Public Transport is hardly the

type of organization that would be expected to make critical comments about

public transit. But this organization, the international equivalent of the

American Public Transportation Association (APTA) put it this way:

In the United States, with the exception of New

York, public transport is unable to compete with the automobile: its speed is

half as fast, which means that door-to-door travel times, incorporating

terminal distance times, waiting and transfer times, are 3 to 4 times longer on

public transport.”

Actually, this is

something of an overstatement. Transit plays an indispensable role in providing

auto-competitive service to a few much focused areas of the nation. But outside

these areas, the potential for transit to attract people out of cars is nearly

non-existent.

This is illustrated by the record of metropolitan areas that

have built new rail systems.

- Between

1990 and 2000, Dallas opened a

commuter rail line and three branches of a light rail system. Yet, overall

transit work trip ridership decreased (Table #2).

- Between

1990 and 2000, St. Louis

opened a new light rail line. Yet, transit work trip ridership decreased

(Table #3).

- Between

1970 and 2000, Washington

opened approximately 100 miles of its Metro system. Yet, transit’s work

trip market share dropped 29 percent.

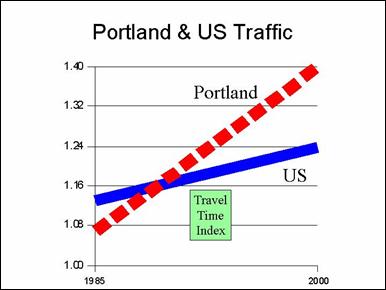

- Transit’s

work trip market share continues to trail pre-light rail levels in Portland,

though minor gains were made in the 1990s. Street and highway traffic has

grown faster than transit use since 1985, the year before the first of two

light rail lines was opened. Traffic delays, as measured by the Travel

Time Index have grown 31 percent, the second largest increase in the

nation (Figure #6).

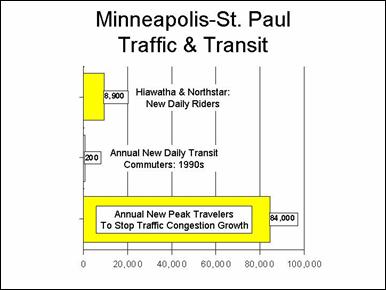

The problem is further illustrated by the case of

Minneapolis-St. Paul, which is currently building a light rail line (the

“Hiawatha Line”) and seeks to build a commuter rail line (the “Northstar

Line”). There, the Texas Transportation Institute estimates that it would take

an addition of 84,000 annual transit one-way

peak period riders just to stop to growth of traffic congestion. The two lines

would add fewer than 9,000 one-way transit riders over a period of 20 years or

more. During the 1990s, transit work trip use increased approximately 200

annually, a small fraction of what would be required to materially impact traffic

congestion (Figure #7).

Urban rail systems

are exceedingly expensive. Often the annual cost per commuter attracted from

the automobile exceeds the recurring lease cost for a new automobile.

|

Table #2

Work Trip Market Share in Dallas County: 1990-2000

|

|

Mode

|

1990

|

Market Share

|

2000

|

Market Share

|

Change

|

Change in Market Share

|

|

Drive Alone

|

718,709

|

76.2%

|

777,372

|

74.8%

|

58,663

|

-1.8%

|

|

Car Pool

|

135,776

|

14.4%

|

167,270

|

16.1%

|

31,494

|

11.9%

|

|

Transit

|

38,150

|

4.0%

|

35,261

|

3.4%

|

(2,889)

|

-16.1%

|

|

Walk

|

19,027

|

2.0%

|

17,390

|

1.7%

|

(1,637)

|

-17.0%

|

|

Other

|

11,004

|

1.2%

|

13,108

|

1.3%

|

2,104

|

8.2%

|

|

Work at Home

|

20,480

|

2.2%

|

28,378

|

2.7%

|

7,898

|

25.8%

|

|

Total

|

943,146

|

100.0%

|

1,038,779

|

100.0%

|

95,633

|

0.0%

|

|

Taxicab included in "Other"

Calculated from US Census Bureau data.

|

|

Table #3

Work Trip Market Share in Metropolitan St. Louis: 1990-2000l

|

|

Mode

|

1990

|

Market Share

|

2000

|

Market Share

|

Change

|

Change in Market Share

|

|

Drive Alone

|

912,509

|

79.7%

|

1,023,627

|

82.6%

|

111,118

|

3.6%

|

|

Car Pool

|

137,883

|

12.0%

|

122,219

|

9.9%

|

(15,664)

|

-18.1%

|

|

Transit

|

31,355

|

2.7%

|

28,675

|

2.3%

|

(2,680)

|

-15.5%

|

|

Walk

|

24,556

|

2.1%

|

20,131

|

1.6%

|

(4,425)

|

-24.3%

|

|

Other

|

10,881

|

1.0%

|

9,020

|

0.7%

|

(1,861)

|

-23.4%

|

|

Work at Home

|

27,152

|

2.4%

|

35,292

|

2.8%

|

8,140

|

20.1%

|

|

Total

|

1,144,336

|

100.0%

|

1,238,964

|

100.0%

|

94,628

|

0.0%

|

|

Taxicab included in "Other"

Calculated from US Census Bureau data.

|

Figure 6

Figure 7

Funding Imbalance

The modest returns from the nation’s new urban rail systems

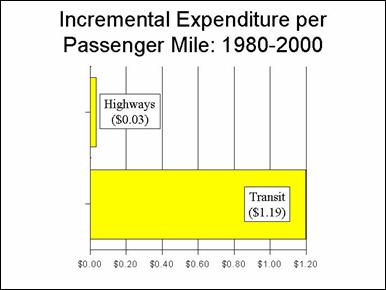

are evident when measured in terms of the cost per new passenger mile. From

1980 to 2000, incremental government expenditures (federal, state and local) on

transit were $1.19 per incremental passenger mile, nearly 40 times that of streets

and highways (Figure #8). And, while highway user fees and special imposts

accounted for 75 percent or more of highway expenditures, transit user fees

accounted for less than 30 percent of expenditures.

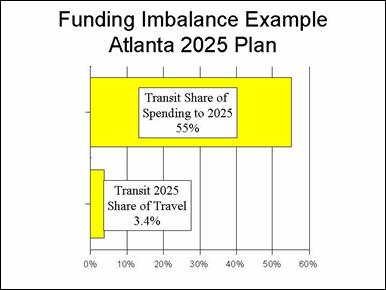

This spending imbalance is even more significant in some of

the nation’s major urban areas. For example, through 2025, the Atlanta

region will spend 55 percent of its transportation resources on public transit,

while transit’s share of trips is expected to grow from only 2.6 percent to 3.4

percent (Figure #9).

Figure 8

Figure 9

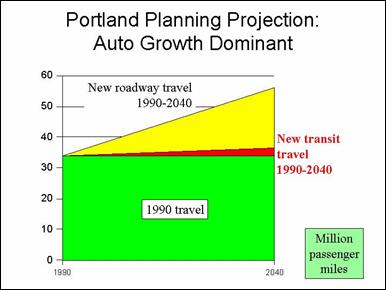

The defining factor with respect to urban transport is that

virtually all new travel demand is expected to be automobile related. Even Portland’s

land use-transport planning agency, Metro, acknowledges this (Figure #10). The

fundamental problem is that there is no transit system that can provide

auto-competitive service to a significant share of destinations outside

downtowns. This is true not only in the United

States, and to a somewhat lesser degree even

in Western Europe. Our research indicates that a transit

system that provides auto-competitive service throughout the modern American

urban area could cost as much as a metropolitan areas’ gross regional product.

Figure 10

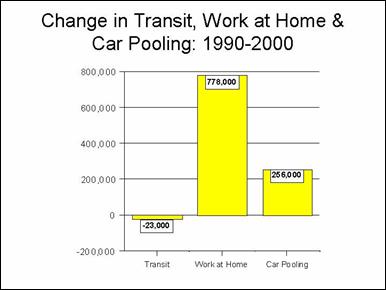

But this does not mean that there is not a cost efficient

role for strategies other than the single occupant automobile. The recent

Census data indicates rays of hope. While overall transit work trip ridership

was declining slightly, progress was made in much less costly modes, namely

working at home (telecommuting) and car pooling. . Working at home increased

778,000 and car pooling increased 256,000, though registering a 3.4 percent

market share loss (Figure #11).

- In

eight metropolitan areas, telecommuting increased more than 25,000. In

each of these areas, the increase was greater than that of transit (Table

#4). Telecommuting increased more than transit in 40 of the nation’s 49

metropolitan areas over 1,000,000, and increased 19 times as much as

transit (Table A-3). Little, if any government subsidy has been used to

encourage telecommuting.

- In 11

metropolitan areas, car pooling increased more than 25,000. Again, in each

such area, the increase was greater than that of transit (Table #5). In

both Atlanta and Dallas-Fort

Worth, which have made major urban rail investments, the 1990s increase in

car pooling alone exceeded the total

transit work trip ridership. Car pooling increased more than transit

in 36 of the nation’s 49 metropolitan areas over 1,000,000 and increased

16 times as much as transit (Table A-3). Some of the metropolitan areas,

such as Atlanta, Phoenix,

Dallas-Fort Worth, Seattle and

Houston employed aggressive

high occupancy vehicle (HOV) lane programs during the 1990s. Regional HOV

lane systems can provide opportunities for improved mobility to the entire

area, not just to downtown. Further, they can and are being used by

transit agencies to provide comparatively low cost express bus services.

The concept can be expanded even further through use of HOT lanes (high

occupancy toll lanes), which permit single occupant vehicles to use HOV

lanes for a price, which can be used to expand the system even further.

Figure 11

|

Table #4

Telecommuting and Transit Work Trip Trend: 1990-2000

|

|

Metropolitan Area

|

Transit Change

|

Telecommuting Change

|

|

New York--Northern New Jersey--Long Island,

NY--NJ--CT--PA CMSA

|

41,472

|

74,500

|

|

Los Angeles--Riverside--Orange County, CA CMSA

|

3,299

|

55,349

|

|

Chicago--Gary--Kenosha, IL--IN--WI CMSA

|

(42,131)

|

40,839

|

|

Atlanta, GA MSA

|

3,286

|

38,742

|

|

Boston--Worcester—Lawrence, MA--NH--ME--CT CMSA

|

29,223

|

33,125

|

|

Dallas--Fort Worth, TX CMSA

|

(567)

|

30,284

|

|

San Francisco--Oakland--San Jose, CA CMSA

|

27,049

|

27,915

|

|

Denver--Boulder--Greeley, CO CMSA

|

17,066

|

25,470

|

|

Total

|

78,697

|

326,224

|

|

Calculated from US

Census data.

|

|

Table #5

Car Pooling and Transit Work Trip Trend: 1990-2000

|

|

Metropolitan Area

|

Transit Change

|

Car Pooling Change

|

|

Atlanta, GA MSA

|

3,286

|

92,022

|

|

Phoenix--Mesa, AZ MSA

|

8,116

|

81,827

|

|

Dallas--Fort Worth, TX CMSA

|

(567)

|

79,603

|

|

Seattle—Tacoma--Bremerton, WA CMSA

|

28,611

|

49,573

|

|

Las Vegas, NV--AZ MSA

|

20,940

|

48,561

|

|

Houston--Galveston--Brazoria, TX CMSA

|

1,643

|

40,049

|

|

Austin--San Marcos, TX MSA

|

3,313

|

32,889

|

|

San Francisco--Oakland--San Jose, CA CMSA

|

27,049

|

28,035

|

|

Denver--Boulder--Greeley, CO CMSA

|

17,066

|

27,499

|

|

Raleigh--Durham--Chapel Hill, NC MSA

|

1,985

|

26,728

|

|

Portland—Salem, OR--WA CMSA

|

22,152

|

25,947

|

|

Total

|

133,594

|

532,733

|

|

Calculated from US

Census data.

|

One of the most promising developments has been the

recognition by the Federal Transit Administration and some transit agencies of

the much more cost effective options for rapid transit using buses. USDOT

research has indicated that bus rapid transit can be five times as cost

efficient per passenger mile.

Smart Growth: More

Traffic Congestion, Less Housing Affordability

The “Smart Growth” movement seeks to stop or control urban

sprawl. Proponents claim that it will reduce traffic congestion, reduce air pollution

and reduce costs. As a result, there are proposals to impose land use

regulations for controlling urban sprawl as in the federal transportation

program. It is fundamental that smart growth and containing sprawl require

higher densities. Smart growth’s goals simply are unattainable without much

higher densities.

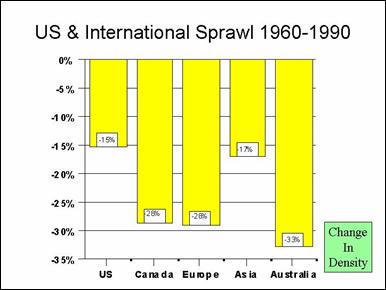

US urban areas tend to be

less densely populated than those in Western Europe and Japan

(Figure #12). But, contrary to the popular view, sprawl is not an American

phenomenon. Sprawl occurs wherever there is population growth and rising

affluence, and European urban areas have seen their urban densities decline at

an even greater rate than in the United States

(Figure #13).

Figure 12

Figure 13

I do not favor sprawl. I favor allowing people to live and

work where and how they like. And, there is no reason not to allow it. Even

today, nearly 400 years after Jamestown,

urbanization accounts for less only 2.6 percent of the nation’s land area.

The claims of the smart growth movement simply do not hold

up.

National and international data clearly indicates that

traffic congestion rises with population density. The higher density European

and Asia urban areas, with their much higher public

transit market shares also have much worse traffic (Figure #14). Research

commissioned by the United States Department of Transportation indicates that

at current US

urban densities, vehicle miles rise more than 80 percent when population

density is doubled. Now, admittedly, that means that per capita driving

declines marginally, but it means that there are more miles in a defined area

--- traffic congestion is worse.

Figure 14

More driving per square mile means that traffic slows down

and that people must spend more time in their cars. Not surprisingly, journey

to work travel times tend to be longer where population densities are higher

--- whether in the United States

or internationally.

And, as traffic volumes in a particular area increase, there

is also an increase in stop and go driving. Slower speeds and stop and go

driving mean greater production of air pollution. So, not surprisingly, air

pollution production tends to be higher where densities are higher. And, it is

well to consider the great progress that has been made in air pollution

abatement in the United States.

In the last 30 years, driving has increased substantially, while criteria air

pollution production has decreased --- not

just per capita --- but overall.

So, smart growth increases traffic congestion, travel times

and air pollution.

Some months ago research was published showing that

transportation costs are higher in more sprawling areas. This is to be

expected. But what may be surprising is that overall household expenditures

tend to be lower where densities are lower. The big factor in this equation is

housing costs. Housing costs are less where densities are less, and they tend

to be less to such a great degree that the transportation cost disadvantage is

more than canceled.

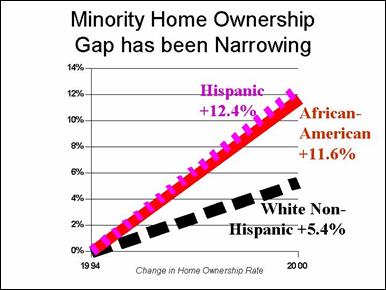

But, the worst impact of all is social. Home ownership is

lower where densities are higher. Thus, smart growth works to make home

ownership more difficult for lower income households. Recent decades shows than

minority home ownership, (African-American and Hispanic), is rising faster than

that of non-Hispanic whites (Figure #15). At the same time, minority home

ownership levels still remain well below that of non-Hispanic whites, which is

why the Bush Administration has undertaken steps to more greatly expand

minority home ownership.

Figure 15

By raising the price of housing, smart growth promotes

social inequity. Smart growth rations land and development. It is a fundamental

principle of economics that when valuable goods are rationed, their prices

rise. When prices rise, it is the lower end of the income spectrum that is

driven away from the market. The lower income spectrum has a disproportionate

representation of minorities. As a result, smart growth reduces home ownership

opportunities for lower income households, especially African-Americans and

Hispanics. There is a raging debate between supporters and opponents of smart

growth about the extent to which home ownership is reduced by smart growth. We often

hear from smart growth supporters that they way to compensate for smart growths

reduction of home ownership is to provide greater amounts of affordable

housing. Such proposals are no more than empty platitudes in view of the fact

that, by some reports, current public resources are sufficient to provide

housing assistance to barely one third of eligible recipients. In fact, recent

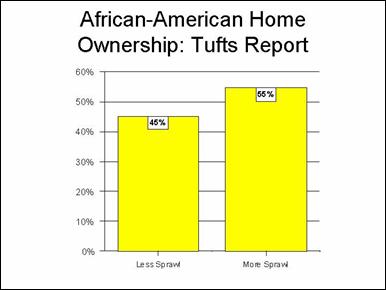

research by Matthew Kahn of Tufts University

indicates that African-American home-ownership tends to be higher in more sprawling

urban areas (Figure #16). Further, research by Edward L. Glaeser and Joseph

Gyourko, published by Harvard University

found that much of the difference in housing affordability around the nation

can be attributed to land regulation.

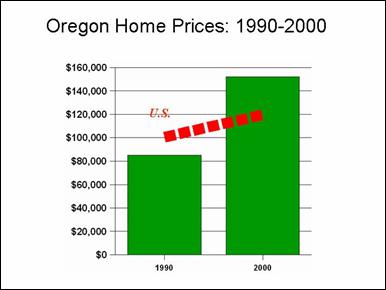

It is not surprising that Oregon,

with the nation’s most comprehensive smart growth regulations, experienced by

far the greatest increase in housing values between 1990 and 2000 (Figure #17).

Figure 16

Figure 17

Thus, smart growth is promises to produce a more traffic

impacted urban area and one that is less economically inclusive. It would be a

mistake for the federal government to encourage such measures through the

transportation program.

RECOMMENDATIONS

Three conclusions

and three recommendations are suggested by the current situation and recent

trends in urban transport.

- The 1990 to 2000 Census data makes it

clear that telecommuting and car pooling options can be far more cost

effective than transit. The General Accounting Office should be asked to

review the potential for more effectively using new transit investment

funds to encourage additional telecommuting and car pooling.

- There is little potential for reducing

traffic congestion or increasing transportation choice for all but a few

through transit. There are no

material successes, US or international. The nation should move toward a

surface transportation program in which new investments are based upon a

policy goal that all can identify with --- the reduction of actual travel

times. Generally, new investments should be made based upon their cost per

reduced hour of actual travel delay.

- Smart growth strategies tend to

intensify the very problems they are purported to solve, especially by

increasing traffic congestion. There should be no federal mandates with

respect to land use or smart growth.

|

Table A-1

Transit Journey to Work Market Share: Major Metropolitan Areas

over 1,000,000: 1990-2000

|

|

Metropolitan Area

|

2000

|

1990

|

Change

|

|

Atlanta, GA MSA

|

3.5%

|

4.6%

|

-24.6%

|

|

Austin--San Marcos, TX MSA

|

2.5%

|

3.2%

|

-21.9%

|

|

Boston--Worcester--Lawrence, MA--NH--ME--CT CMSA

|

8.8%

|

9.7%

|

-8.8%

|

|

Buffalo--Niagara Falls, NY MSA

|

3.3%

|

4.5%

|

-24.8%

|

|

Charlotte--Gastonia--Rock Hill, NC--SC MSA

|

1.3%

|

1.7%

|

-24.8%

|

|

Chicago--Gary--Kenosha, IL--IN--WI CMSA

|

11.2%

|

13.4%

|

-16.4%

|

|

Cincinnati--Hamilton, OH--KY--IN CMSA

|

2.8%

|

3.6%

|

-20.3%

|

|

Cleveland--Akron, OH CMSA

|

3.3%

|

4.5%

|

-26.0%

|

|

Columbus, OH MSA

|

2.2%

|

2.7%

|

-17.1%

|

|

Dallas--Fort Worth, TX CMSA

|

1.7%

|

2.3%

|

-22.8%

|

|

Denver--Boulder--Greeley, CO CMSA

|

4.3%

|

4.0%

|

8.3%

|

|

Detroit--Ann Arbor--Flint, MI CMSA

|

1.7%

|

2.2%

|

-22.8%

|

|

Grand Rapids--Muskegon--Holland, MI MSA

|

0.8%

|

1.0%

|

-26.4%

|

|

Greensboro--Winston-Salem--High Point, NC MSA

|

0.8%

|

1.0%

|

-27.7%

|

|

Hartford, CT MSA

|

2.8%

|

3.6%

|

-23.3%

|

|

Houston--Galveston--Brazoria, TX CMSA

|

3.2%

|

3.7%

|

-13.3%

|

|

Indianapolis, IN MSA

|

1.3%

|

2.0%

|

-35.7%

|

|

Jacksonville, FL MSA

|

1.3%

|

2.0%

|

-32.5%

|

|

Kansas City, MO--KS MSA

|

1.2%

|

2.0%

|

-40.9%

|

|

Las Vegas, NV--AZ MSA

|

4.0%

|

1.9%

|

111.9%

|

|

Los Angeles--Riverside--Orange County, CA CMSA

|

4.6%

|

4.5%

|

1.7%

|

|

Louisville, KY--IN MSA

|

2.2%

|

3.1%

|

-30.9%

|

|

Memphis, TN—AR--MS MSA

|

1.7%

|

2.8%

|

-39.9%

|

|

Miami--Fort Lauderdale, FL CMSA

|

3.8%

|

4.2%

|

-10.8%

|

|

Milwaukee--Racine, WI CMSA

|

3.9%

|

4.8%

|

-18.8%

|

|

Minneapolis--St. Paul, MN--WI MSA

|

4.4%

|

5.2%

|

-15.6%

|

|

Nashville, TN MSA

|

0.9%

|

1.6%

|

-45.2%

|

|

New Orleans, LA MSA

|

5.3%

|

7.0%

|

-23.9%

|

|

New York--Northern New Jersey--Long Island,

NY--NJ--CT--PA CMSA

|

24.1%

|

25.8%

|

-6.5%

|

|

Norfolk--Virginia Beach--Newport News, VA--NC MSA

|

1.8%

|

2.1%

|

-15.4%

|

|

Oklahoma City, OK MSA

|

0.5%

|

0.6%

|

-10.8%

|

|

Orlando, FL MSA

|

1.6%

|

1.4%

|

10.6%

|

|

Philadelphia--Wilmington--Atlantic City, PA--NJ--DE--MD CMSA

|

8.6%

|

10.1%

|

-14.6%

|

|

Phoenix--Mesa, AZ MSA

|

1.9%

|

2.0%

|

-4.6%

|

|

Pittsburgh, PA MSA

|

6.1%

|

7.9%

|

-22.4%

|

|

Portland--Salem, OR--WA CMSA

|

5.7%

|

4.8%

|

18.2%

|

|

Providence--Fall River--Warwick, RI--MA MSA

|

2.4%

|

2.5%

|

-5.2%

|

|

Raleigh—Durham--Chapel Hill, NC MSA

|

1.5%

|

1.8%

|

-17.9%

|

|

Rochester, NY MSA

|

1.9%

|

3.1%

|

-38.4%

|

|

Sacramento--Yolo, CA CMSA

|

2.7%

|

2.4%

|

13.0%

|

|

Salt Lake City--Ogden, UT MSA

|

3.0%

|

3.0%

|

0.1%

|

|

San Antonio, TX MSA

|

2.8%

|

3.6%

|

-21.7%

|

|

San Diego, CA MSA

|

3.3%

|

3.2%

|

3.2%

|

|

San Francisco--Oakland--San Jose, CA CMSA

|

9.4%

|

9.2%

|

1.8%

|

|

Seattle--Tacoma--Bremerton, WA CMSA

|

6.7%

|

6.1%

|

9.2%

|

|

St. Louis, MO--IL MSA

|

2.3%

|

2.8%

|

-18.4%

|

|

Tampa--St. Petersburg--Clearwater, FL MSA

|

1.3%

|

1.3%

|

-5.3%

|

|

Washington--Baltimore, DC--MD--VA--WV CMSA

|

9.2%

|

11.3%

|

-18.7%

|

|

West Palm Beach--Boca Raton, FL MSA

|

1.2%

|

1.1%

|

7.9%

|

|

Average

|

3.8%

|

4.3%

|

-12.3%

|

|

Taxicabs excluded

Minor geographical differences between 1990

and 2000

Calculated from US Census Bureau data.

|

|

Table A-2

Work Trip Travel Times: Major Metropolitan Areas Over

1,000,000: 2000 by Mode

|

|

Metropolitan Area

|

Mean Travel Time

(Minutes)

|

Travel Time: Not Public Transit (Mainly auto)

|

Travel Time: Public Transit

|

Transit Time Compared to Other

|

|

Atlanta, GA MSA

|

31.2

|

30.5

|

50.3

|

1.65

|

|

Austin--San Marcos, TX MSA

|

25.5

|

25.2

|

37.9

|

1.50

|

|

Boston--Worcester--Lawrence, MA--NH--ME--CT CMSA

|

27.8

|

26.1

|

43.8

|

1.68

|

|

Buffalo--Niagara Falls, NY MSA

|

21.1

|

20.5

|

36.2

|

1.76

|

|

Charlotte--Gastonia--Rock Hill, NC--SC MSA

|

26.1

|

25.9

|

44.1

|

1.71

|

|

Chicago--Gary--Kenosha, IL--IN--WI CMSA

|

31.0

|

28.5

|

49.7

|

1.75

|

|

Cincinnati--Hamilton, OH--KY—IN CMSA

|

24.3

|

23.9

|

38.4

|

1.61

|

|

Cleveland--Akron, OH CMSA

|

24.0

|

23.3

|

42.9

|

1.84

|

|

Columbus, OH MSA

|

23.2

|

22.9

|

35.6

|

1.56

|

|

Dallas--Fort Worth, TX CMSA

|

27.5

|

27.1

|

48.7

|

1.80

|

|

Denver--Boulder--Greeley, CO CMSA

|

25.9

|

25.1

|

42.7

|

1.70

|

|

Detroit--Ann Arbor--Flint, MI CMSA

|

26.1

|

25.7

|

46.0

|

1.79

|

|

Grand Rapids--Muskegon--Holland, MI MSA

|

20.7

|

20.6

|

32.2

|

1.56

|

|

Greensboro--Winston-Salem--High Point, NC MSA

|

22.4

|

22.2

|

36.8

|

1.66

|

|

Hartford, CT MSA

|

22.9

|

22.5

|

37.7

|

1.67

|

|

Houston--Galveston--Brazoria, TX CMSA

|

28.8

|

28.0

|

50.4

|

1.80

|

|

Indianapolis, IN MSA

|

23.8

|

23.6

|

40.6

|

1.72

|

|

Jacksonville, FL MSA

|

26.6

|

26.3

|

47.2

|

1.80

|

|

Kansas City, MO--KS MSA

|

22.9

|

22.7

|

38.6

|

1.70

|

|

Las Vegas, NV--AZ MSA

|

24.1

|

22.9

|

51.3

|

2.24

|

|

Los Angeles--Riverside--Orange County, CA CMSA

|

29.1

|

28.0

|

50.0

|

1.79

|

|

Louisville, KY--IN MSA

|

22.7

|

22.4

|

37.4

|

1.67

|

|

Memphis, TN--AR--MS MSA

|

24.5

|

24.2

|

44.9

|

1.86

|

|

Miami--Fort Lauderdale, FL CMSA

|

28.9

|

28.0

|

50.2

|

1.79

|

|

Milwaukee--Racine, WI CMSA

|

22.1

|

21.3

|

39.9

|

1.87

|

|

Minneapolis--St. Paul, MN--WI MSA

|

23.7

|

23.0

|

36.2

|

1.57

|

|

Nashville, TN MSA

|

25.8

|

25.6

|

41.2

|

1.61

|

|

New Orleans, LA MSA

|

26.7

|

25.7

|

43.6

|

1.70

|

|

New York--Northern New Jersey--Long Island,

NY--NJ--CT--PA CMSA

|

34.0

|

27.8

|

52.2

|

1.88

|

|

Norfolk--Virginia Beach--Newport News, VA--NC MSA

|

24.1

|

23.8

|

43.5

|

1.83

|

|

Oklahoma City, OK MSA

|

22.0

|

21.9

|

31.4

|

1.43

|

|

Orlando, FL MSA

|

27.0

|

26.6

|

48.2

|

1.82

|

|

Philadelphia--Wilmington--Atlantic City, PA--NJ--DE--MD CMSA

|

27.9

|

25.9

|

47.4

|

1.83

|

|

Phoenix--Mesa, AZ MSA

|

26.1

|

25.7

|

45.3

|

1.76

|

|

Pittsburgh, PA MSA

|

25.3

|

24.4

|

38.8

|

1.59

|

|

Portland--Salem, OR--WA CMSA

|

24.4

|

23.3

|

40.7

|

1.75

|

|

Providence--Fall River--Warwick, RI--MA MSA

|

23.2

|

22.6

|

47.0

|

2.08

|

|

Raleigh--Durham--Chapel Hill, NC MSA

|

24.9

|

24.7

|

33.0

|

1.34

|

|

Rochester, NY MSA

|

21.1

|

20.8

|

37.0

|

1.78

|

|

Sacramento--Yolo, CA CMSA

|

25.6

|

25.1

|

42.5

|

1.69

|

|

Salt Lake City--Ogden, UT MSA

|

22.4

|

21.7

|

42.4

|

1.95

|

|

San Antonio, TX MSA

|

24.5

|

23.9

|

44.3

|

1.85

|

|

San Diego, CA MSA

|

25.3

|

24.4

|

50.5

|

2.07

|

|

San Francisco--Oakland--San Jose, CA CMSA

|

29.3

|

27.5

|

46.0

|

1.67

|

|

Seattle--Tacoma--Bremerton, WA CMSA

|

27.7

|

26.4

|

44.8

|

1.70

|

|

St. Louis, MO--IL MSA

|

25.5

|

25.0

|

44.3

|

1.77

|

|

Tampa--St. Petersburg--Clearwater, FL MSA

|

25.6

|

25.4

|

41.1

|

1.62

|

|

Washington--Baltimore, DC--MD--VA--WV CMSA

|

31.7

|

30.0

|

47.1

|

1.57

|

|

West Palm Beach--Boca Raton, FL MSA

|

25.7

|

25.4

|

45.6

|

1.79

|

|

Average

|

25.6

|

24.8

|

43.0

|

1.74

|

|

Minor geographical differences between 1990

and 2000

Calculated from US Census Bureau data.

|

|

Table A-3

Change in Transit, Car Pools and Work at Home: Metropolitan

Areas Over 1,000,000: 1990-2000

|

|

Metropolitan Area

|

New Transit Trips

|

New Carpool Trips

|

New Work at Home

|

|

Atlanta, GA MSA

|

3,286

|

92,022

|

38,742

|

|

Austin--San Marcos, TX MSA

|

3,313

|

32,889

|

11,443

|

|

Boston--Worcester--Lawrence, MA--NH--ME--CT CMSA

|

29,223

|

9,556

|

33,125

|

|

Buffalo--Niagara Falls, NY MSA

|

(6,228)

|

(10,484)

|

1,085

|

|

Charlotte--Gastonia--Rock Hill, NC--SC MSA

|

(675)

|

9,108

|

9,592

|

|

Chicago--Gary--Kenosha, IL--IN--WI CMSA

|

(42,131)

|

3,668

|

40,839

|

|

Cincinnati--Hamilton, OH--KY--IN CMSA

|

(1,923)

|

2,514

|

8,941

|

|

Cleveland--Akron, OH CMSA

|

(10,089)

|

(7,408)

|

12,217

|

|

Columbus, OH MSA

|

(880)

|

(2,501)

|

7,417

|

|

Dallas--Fort Worth, TX CMSA

|

(567)

|

79,603

|

30,284

|

|

Denver--Boulder--Greeley, CO CMSA

|

17,066

|

27,499

|

25,470

|

|

Detroit--Ann Arbor--Flint, MI CMSA

|

(7,424)

|

2,309

|

17,330

|

|

Grand Rapids--Muskegon--Holland, MI MSA

|

(102)

|

8,555

|

5,517

|

|

Greensboro--Winston-Salem--High Point, NC MSA

|

(487)

|

9,415

|

4,555

|

|

Hartford, CT MSA

|

(4,425)

|

(11,830)

|

3,463

|

|

Houston--Galveston--Brazoria, TX CMSA

|

1,643

|

40,049

|

15,304

|

|

Indianapolis, IN MSA

|

(2,220)

|

2,898

|

8,424

|

|

Jacksonville, FL MSA

|

(1,731)

|

2,875

|

546

|

|

Kansas City, MO--KS MSA

|

(5,097)

|

(4,538)

|

8,724

|

|

Las Vegas, NV--AZ MSA

|

20,940

|

48,561

|

10,980

|

|

Los Angeles--Riverside--Orange County, CA CMSA

|

3,299

|

(23,904)

|

55,349

|

|

Louisville, KY--IN MSA

|

(3,344)

|

(3,225)

|

2,884

|

|

Memphis, TN--AR--MS MSA

|

(3,876)

|

5,834

|

4,489

|

|

Miami--Fort Lauderdale, FL CMSA

|

(468)

|

7,019

|

16,509

|

|

Milwaukee--Racine, WI CMSA

|

(5,279)

|

(3,788)

|

3,473

|

|

Minneapolis--St. Paul, MN--WI MSA

|

1,993

|

13,106

|

16,186

|

|

Nashville, TN MSA

|

(2,500)

|

10,959

|

7,245

|

|

New Orleans, LA MSA

|

(5,622)

|

4,829

|

4,874

|

|

New York--Northern New Jersey--Long Island,

NY--NJ--CT--PA CMSA

|

41,472

|

(5,455)

|

74,500

|

|

Norfolk--Virginia Beach--Newport News, VA--NC MSA

|

(1,150)

|

(6,768)

|

(16,959)

|

|

Oklahoma City, OK MSA

|

22

|

1,470

|

3,183

|

|

Orlando, FL MSA

|

4,521

|

21,112

|

11,624

|

|

Philadelphia--Wilmington--Atlantic City, PA--NJ--DE--MD CMSA

|

(39,509)

|

(49,806)

|

16,727

|

|

Phoenix--Mesa, AZ MSA

|

8,116

|

81,827

|

24,390

|

|

Pittsburgh, PA MSA

|

(10,708)

|

(19,347)

|

5,934

|

|

Portland--Salem, OR--WA CMSA

|

22,152

|

25,947

|

18,518

|

|

Providence--Fall River--Warwick, RI--MA MSA

|

(452)

|

(8,296)

|

2,082

|

|

Raleigh--Durham--Chapel Hill, NC MSA

|

1,985

|

26,728

|

12,180

|

|

Rochester, NY MSA

|

(5,092)

|

(8,774)

|

3,204

|

|

Sacramento--Yolo, CA CMSA

|

5,140

|

14,426

|

10,941

|

|

Salt Lake City--Ogden, UT MSA

|

4,842

|

17,392

|

9,399

|

|

San Antonio, TX MSA

|

(809)

|

18,708

|

4,831

|

|

San Diego, CA MSA

|

3,535

|

14

|

(4,103)

|

|

San Francisco--Oakland--San Jose, CA CMSA

|

27,049

|

28,035

|

27,915

|

|

Seattle--Tacoma--Bremerton, WA CMSA

|

28,611

|

49,573

|

22,138

|

|

St. Louis, MO--IL MSA

|

(3,763)

|

(15,664)

|

8,140

|

|

Tampa--St. Petersburg--Clearwater, FL MSA

|

1,233

|

10,207

|

12,576

|

|

Washington--Baltimore, DC--MD--VA--WV CMSA

|

(32,046)

|

(28,430)

|

(39,622)

|

|

West Palm Beach--Boca Raton, FL MSA

|

1,528

|

8,134

|

9,284

|

|

Total

|

32,372

|

506,623

|

621,889

|

|

Compared to Transit

|

|

16

|

19

|

|

Minor geographical differences between 1990

and 2000

Calculated from US Census Bureau data.

|

The Heritage

Foundation

The Heritage Foundation

is a public policy, research, and educational organization operating under

Section 501(C)(3). It is privately supported, and receives no funds from any

government at any level, nor does it perform any government or other contract

work.

The Heritage Foundation

is the most broadly supported think tank in the United States. During 2001, it had more than 200,000

individual, foundation, and corporate supporters representing every state in

the U.S. Its 2001 contributions came from the following

sources:

Individuals 60.93%

Foundations 27.02%

Corporations 7.61%

Investment Income 1.60%

Publication Sales and Other 2.84%

The top five corporate

givers provided The Heritage Foundation with less than 3.5% of its 2001 income.

The Heritage Foundation’s books are audited annually by the national accounting

firm of Deloitte & Touche. A list of major donors is available from The

Heritage Foundation upon request.

Members of The Heritage

Foundation staff testify as individuals discussing their own independent

research. The views expressed are their own, and do not reflect an

institutional position for The Heritage Foundation or its board of trustees.

The Public Purpose: One of National Journal's Top 4 Transport Internet Sites

|

NAVIGATION & PUBLICATION SERIES

|

The Public Purpose WENDELL COX CONSULTANCY

Demographia

P. O. Box 841 - Belleville, IL 62269 USA

Telephone: +1.618.632.8507 -

Facsimile: +1.810.821.8134

|

To facilitate the ideal of government as the servant of the people

by identifying and implementing

strategies to achieve public purposes

at a cost that is no higher than necessary.

|

|